If you have ever complained about paying high taxes, here’s a simple tip that will help you save some money on taxes and prepare for your retirement at the same time.

Sounds good? What I am talking about is a less commonly known program called the Supplementary Retirement Scheme (SRS).

This is voluntary saving scheme that the Government started in 2001 to encourage people to save for their retirement by offering tax benefits. The idea was to encourage people to create a secondary source of retirement funds to complement their CPF savings.

How does SRS help me save money on taxes?

1) The amount you set aside in SRS gets deducted off your taxable salary for that year. This lowers your tax bracket and therefore reduces the amount of tax payable.

Do note that there is a limit to how much you can contribute each year. For Singaporean and PRs, the maximum you can contribute to SRS per year is currently $15,300, for foreigners the amount is higher at $35,700.

So how much tax savings can I enjoy?

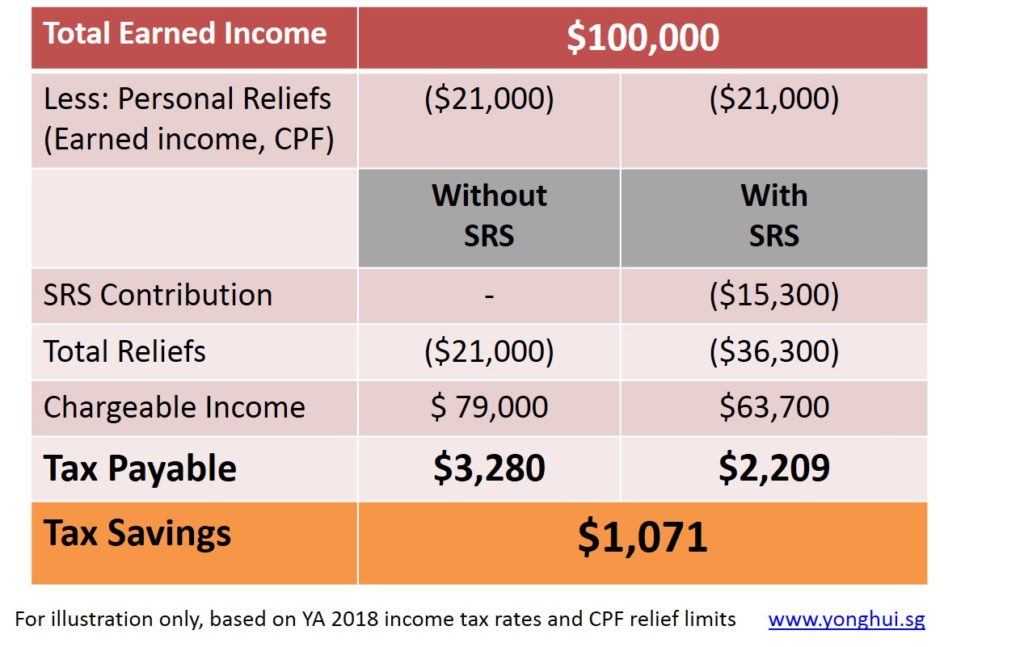

Let’s take a look at an example below of the tax savings for a single lady who earns an annual income of $100k.

By setting aside $15,300 in SRS, she enjoys a tax saving of $1,071 which works out to 32% saving in her taxes for the year!

By setting aside $15,300 in SRS, she enjoys a tax saving of $1,071 which works out to 32% saving in her taxes for the year!

2) The money in your SRS account will accumulate tax-free until you retire. If you withdraw money from your SRS account after the statutory retirement age (currently at 62), only 50% of what you withdraw will be taxed.

You can enjoy further tax savings if you choose to stagger your withdrawals over the period of 10 years instead of withdrawing all your savings in a lump sum.

What is the catch?

1) Early Withdrawal Penalty

Because SRS is designed to help you save for your retirement, if you make any withdrawals before the statutory retirement age, you will be taxed on the full amount. On top of that, you would also incur an additional premature withdrawal penalty of 5%.

So, it’s best to ensure that whatever money you put in your SRS account is what you do not need in the near future.

2) Returns

Unlike CPF that gives a return of 2.5% for OA and 4% for SA, the SRS account is a normal bank account, earning typical bank interest rates of just 0.05% p.a.

Hence it’s crucial to invest your SRS funds to stay ahead of inflation plus grow it over time for your retirement.

Some people have a misconception that there’s limited investment options to invest their SRS funds. In fact, you can invest in a wide array of investment vehicles, including stocks, unit trusts, ETFs, even accredited investor funds (through selected platforms)

How to participate in SRS

- Open an SRS account with any of the 3 local banks, POSB/DBS, UOB, OCBC. You can decide how much to put in, up to the annual contribution limit.

- Next, look for suitable vehicles to grow your SRS funds for your retirement be it to accumulate a nest egg or generate retirement income.

Take note that in order to qualify for tax savings next year, you need to put money into your SRS account before the end of this year. So now’s the time to act on this if you have not already done so!

* This article was first published in 2013 and has been updated for relevance and accuracy

To Your Success and Happiness,

Yong Hui

Hey thanks so much for these tips… :)