Tax season is here again, the time of the year when we have to file our taxes and feel the pinch when we receive the tax bills.

Singapore’s income tax system is progressive, so the more you earn, the more you will be taxed. For example, an executive earning $100k a year will be looking at taxes of $5,650 before any reliefs while a director earning $320,000/yr can pay as much as $44,450 in taxes.

The good news is there are various tax relief initiatives you can leverage to save money off your taxes.

Here are 5 tax reliefs that can help you legally reduce your income tax

1. Contribute to Supplementary Retirement Scheme (SRS)

The Supplementary Retirement Scheme (SRS) is a voluntary scheme to encourage individuals to save for retirement. The amount you set aside in SRS gets deducted from your taxable salary for that year. This lowers your tax bracket and therefore reduces the amount of tax payable.

The SRS scheme is not related to CPF and applies to Singapore, PR as well as foreigners. You can contribute at any time, and as often as you like, subject to the maximum SRS contribution for the year.

For Singaporean and PRs, the maximum you can contribute to SRS per year is currently $15,300, for foreigners the amount is higher at $35,700.

So how much can it save you in taxes?

Let’s look at 2 examples

Example 1: Singaporean earning $120k with $20k personal reliefs and contributing the maximum $15,300 to his SRS account

Screenshot generated using the OCBC SRS calculator at https://www.ocbc.com/personal-banking/investments/supplementary-retirement-scheme-account

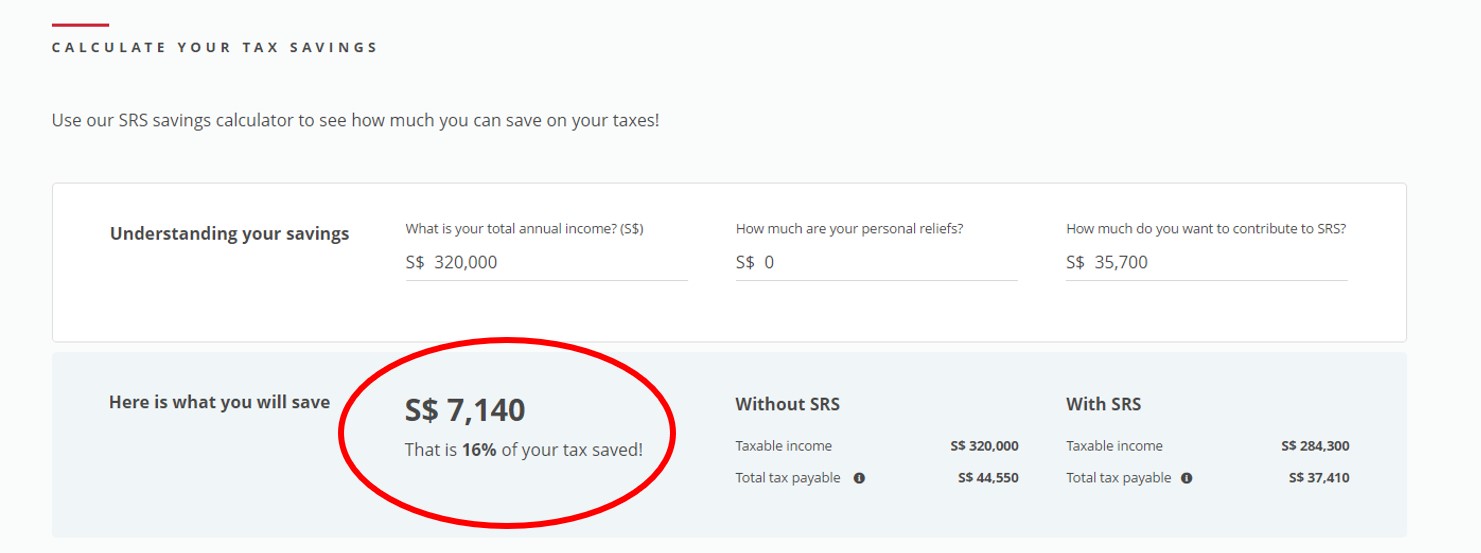

Example 2: An expat earning $320k and setting aside $35,700 in his SRS account

Screenshot generated using the OCBC SRS calculator at https://www.ocbc.com/personal-banking/investments/supplementary-retirement-scheme-account

As you can see, contributing to SRS can provide a healthy reduction in taxes.

In particular, the higher SRS contribution limit can generate significant savings for expats who do not enjoy any CPF relief.

Plus, you can grow your SRS funds by investing in a wide range of investment, including stocks, ETFs, unit trusts and even Accredited Investor funds (to find out more, contact me).

Now, people always ask me, “What’s the catch?”

I wrote more about it here.

Essentially, SRS is meant to support your retirement so any withdrawals made before the prescribed retirement age* will be subjected to a 5% penalty and be taxed in full.

If you only withdraw after the prescribed retirement age, there is no penalty and you will only be taxed on 50% of the withdrawn amount. You can also stagger your withdrawal over 10 years to reduce the impact of tax.

* The prescribed retirement age refers to the statutory retirement age prevailing at the time of an SRS member’s first contribution. Currently the statutory retirement age is 63.

10 yr holding period for foreigners

This is one concession that many foreigners are not aware of.

Foreigners can actually make a one-time full withdrawal of their SRS funds without penalty, so long as they have maintained their SRS account for at least 10 years from their first contribution.

So if you are an expat working in Singapore, it means the earlier you start contributing to SRS, the earlier you can withdraw the funds in full without penalty. Do note that 50% of the amount fully withdrawn is subject to tax.

If you had contributed to SRS before 31st Dec 2022, the amount you contributed will automatically be reflected in your tax filing form by your SRS operator (DBS/UOB/OCBC).

For those who are just starting to contribute to SRS this year, the contributions made before 31st Dec 2023 will be reflected as tax reliefs for the next tax filing year 2024.

2. Top up your CPF and that of your parents (only for Singaporeans and PRs with CPF account)

Singaporeans and PRs employees can enjoy further tax relief through CPF top ups.

Personal CPF Top up: You can top up your CPF Special/Retirement Account and/or Medisave Account and enjoy a tax relief of up to $8,000/yr.

Take note that the CPF Top Up applies only up to the current Full Retirement Sum (FRS). This stands at $213,000 in 2025. If you have already hit the FRS, you will not enjoy any tax relief from the top up.

CPF Top Up for loved ones e.g parents or grandparents: You can enjoy a further tax relief of $8,000/yr by topping up the CPF Special/Retirement Account and/or Medisave Account of your loved ones.

Any top ups made this year will translate to tax reliefs next year.

3. Take a course to upgrade your skills

You can also get tax relief of up to S$5,500 on courses that you have attended in 2024, as long as the course is relevant for your employment and if you can prove that you have paid for it yourself.

If you have taken a course that will enable you to switch careers, you can still claim it.

Do note that any amount paid or reimbursed by your employer or any other organisations (including the use of SkillsFuture Credit) cannot be claimed as Course Fees Relief.

4. Claim life insurance relief

Up to $5,000 tax relief can be claimed on the premiums that you have paid for your own or the life insurance policy of your spouse.

However note that if you are a Singaporean or PR whose total compulsory employee CPF contributions exceed $5,000, you will not be entitled to claim this relief.

That’s why it’s particularly useful for expats who do not contribute to CPF.

5. Make a charity donation

Enjoy additional tax savings by doing good and making a charity donation. Simply make a donation to any charity that is registered as an IPC (Institute of a Public Character) to enjoy 250% in tax deductions based on the amount donated, valid till 31 December 2026

Some examples of IPC are Community Chest, Singapore Cancer Society, MINDS, Club Rainbow, even NUS (if you are an alumni)

If you have made charity donations last year, you can enjoy $2.50 deducted off your taxable income for every $1 you donate in this year’s tax filing.

Otherwise you can always start donating this year to enjoy tax deduction off your taxes next year.

For more information

To find out more about the tax reliefs you are eligible for, check out the IRAS website below.

Do also take note that a personal income tax relief cap of $80,000 applies to the total amount of all tax reliefs claimed for each Year of Assessment.

Hope the above helps and remember to file your taxes soon!

To Your Success and Happiness,

Yong Hui