This part 2 post is especially written for you if you are 40 and above this year and wondering if and how will CareShield Life impact you. If you are turning 30-40 next year, do check out my previous article about CareShield Life.

Some of my clients in their 40s ask me “What is this CareShield Life about? Do I need to do anything if I already have ElderShield?”

What is CareShield Life?

CareShield Life is a national healthcare scheme to help Singaporeans and PRs cope with the cost of long-term disability care.

How different is CareShield Life from ElderShield?

Basically, CareShield Life is an enhanced version of the current ElderShield scheme to provide better coverage.

(Don’t know what is ElderShield about? Find out more about ElderShield here).

Benefit wise, CareShield Life has 3 key enhancements over ElderShield

1. Lifetime Cash Payouts

CareShield Life offers lifetime cash payouts which is a big improvement over the limited 6 year payout under ElderShield 400 and 5 years payout under ElderShield 300.

2. Higher monthly payout that increases over time

The monthly payout is higher, starting from $600/mth compared to $400/mth for ElderShield 400. Payouts also increase every year until age 67 or until claim, whichever is earlier.

3. Universal Coverage

CareShield Life will cover all Singaporeans and PR regardless of any pre-existing severe disabilities they already have.

However as with most things in life, with higher benefits comes higher costs.

-

Higher Premiums

Premiums of CareShield Life will be higher than ElderShield. For example, a male who enrolled to the current ElderShield scheme at the starting age of 40 pays $175/yr while CareShield Life premium for a 40 yr old is $318.

However, the government will provide some subsidies and participation incentives for switching over from ElderShield which will help manage the increase. Both ElderShield and CareShield Life premiums are payable using Medisave.

-

Premiums increases over time

ElderShield’s premium is fixed based on the entry age and so is the monthly payout.

In comparison, CareShield Life’s premiums will increase with age because of the increase in payout every year. The rate of increase of both premiums and payout will be guaranteed at 2% per year for the first 5 years and thereafter will vary depending on the adjustment each year.

-

Longer Premium payment term

ElderShield premiums are payable from age 40-65, while CareShield Life starts from age 30 and ends at age 67.

So how will CareShield Life affect me?

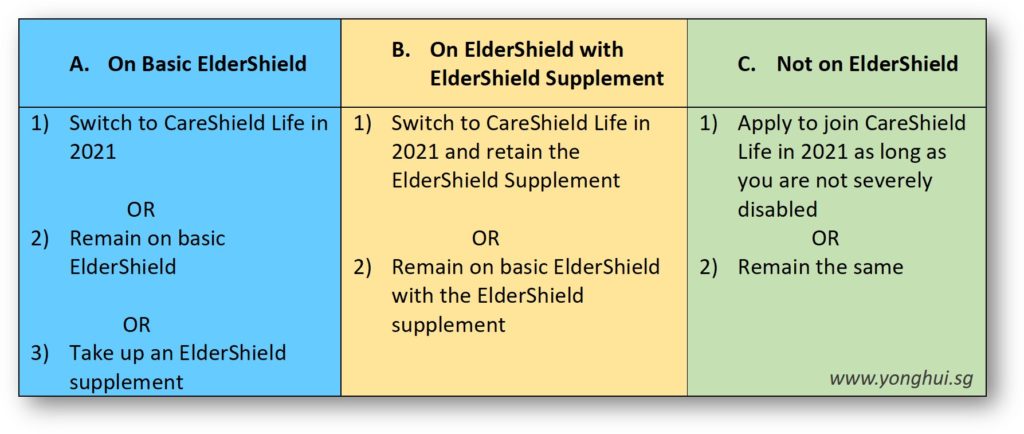

That depends on which category you are in.

If you are aged 40 and above this year, you will likely fall under one of the 3 categories below.

Which group are you in?

Group A. You are on basic ElderShield scheme

Basically you did nothing after you turned 40 so you were automatically enrolled in ElderShield and paying the premiums through your Medisave.

Depending on your age, you will be either under the ElderShield 400 scheme which gives a payout of $400/mth for 6 years or under ElderShield 300 which pays $300/mth for 5 years in the event of severe disability.

Group B. You had previously purchased an ElderShield Supplement

On top of ElderShield, you also have an ElderShield supplement from one of the 3 appointed private insurers – Aviva, Great Eastern or NTUC that provides you with a higher monthly payout and an extended payout period.

Group C. You are not on basic ElderShield

You may have previously opted out of ElderShield or was unable to get covered due to medical reasons. Another group could fall under those whose turned 40 yrs old before ElderShield scheme started in 2002.

*If you are not sure which category you belong to, you can log in to CPF to check your coverage or speak to a financial advisor.

The table below shows the options you have depending on the category you fall under.

Basically, existing ElderShield policyholders will have an option to switch to CareShield Life from 2021 to get the enhanced benefits.

Upon switching, ElderShield 400 policyholders will pay a base CareShield premium depending on your age.

ElderShield 300 policyholders and those not currently insured by ElderShield will need to pay an additional catch up component for the 10 years. You can check the premiums using the CareShield Life calculator here https://www.moh.gov.sg/careshieldlife/about-careshield-life/careshield-life-premium-calculator

You can also choose to maintain status quo and remain on the ElderShield scheme.

In that case, you will continue to get the same benefits and pay the same premiums.

The government will take over the administration of the ElderShield scheme fro 2021 instead of the private insurers.

To switch or not to switch, that’s the question..

It really depends on individual preference and situation.

In my personal opinion, if you are currently on basic ElderShield scheme with no ElderShield supplements, the increased coverage in CareShield Life will come in handy, especially the lifetime payout support. Do note though that you can only change to CareShield Life in 2021.

Alternatively, if you find the basic ElderShield $400/mth payout or even CareShield Life’s $600/mth payout insufficient, consider enhancing your ElderShield benefits with an ElderShield supplement that can immediately increase your monthly payout and payout duration.

If you already have an existing ElderShield supplement that pays you a much higher payout e.g $1,600 or $2,000/mth for a lifetime, then the increase in Careshield Life benefits may not be very significant compared to what you already have.

Hope this article has given you more clarity and perspective about CareShield Life. Should you have questions or like some advice regarding your individual situation, contact me here.

To Your Success and Happiness,

Yong Hui