Parenthood is a phase of life where demands are high and resources like time and money are limited.

Out of love, many parents choose to put their children’s needs above their own and sacrifice their personal needs. However, if we truly want the best for our children, I personally feel we as mothers need to take good care of ourselves too. And it is possible to find the balance.

This May as we celebrate Mother’s Day, I am dedicating this article to enhance the financial well-being of all the wonderful mothers out there.

You are Important and You Matter 💖

1. Take care of your own financial protection first

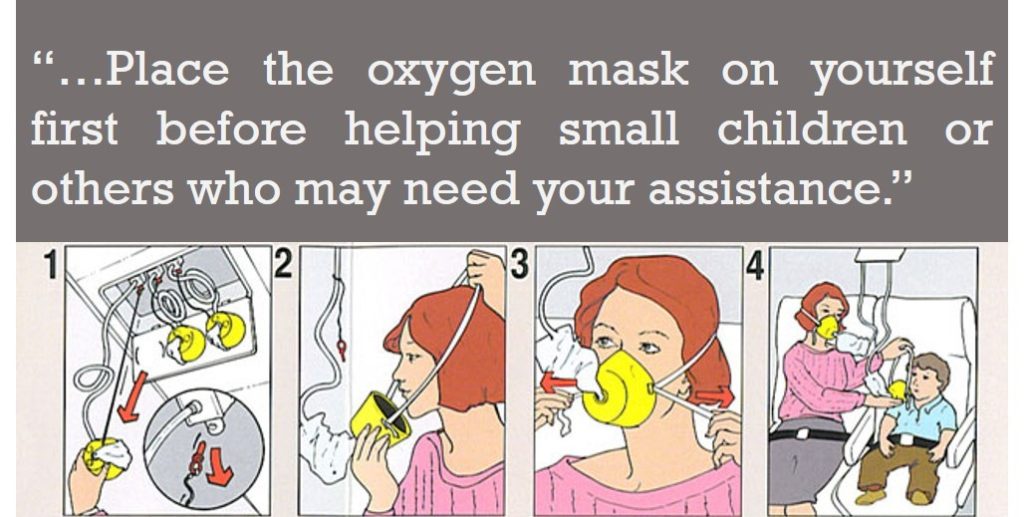

On airplanes, we were asked to put on our own oxygen mask first before helping small children or others. Likewise, financially we need to first ensure our own protection is in place before getting insurance for our children.

Our children are dependent on us for everything, especially young children. As mothers, we are not only their emotional caregivers, we are their financial supporters as well, especially in dual income families or single parent homes.

If we are unable to work due to an illness or accident, our child loses a pillar of financial support which will directly impact their lives. On top of that, there are hefty medical bills to be paid, creating even greater financial burden and stress to the family.

If we want to provide for our children, we must first ensure that we ourselves have adequate insurance protection.

3 essential types of insurance that mothers need

1) Comprehensive Hospitalisation cover

2) Critical Illness Protection

3) Income and Disability Protection

If you do have some insurance policies but are unsure if they are adequate and would like some advice, this will help.

2. Plan for your own future

As mothers, we always have the best interests of our children at heart. We want them to be healthy and happy. We want to provide them with a good life and a good future.

These days, there are so many enrichment programs out there, from art to music to swimming, even taekwando. And not to mention the academic ones for reading & writing, chinese, maths etc.

So many parents end up spending hundreds of dollars each month on enrichment classes and tuition programs, in the hope that their children can excel in their studies and reach their fullest potential.

On top of that, parents also take up education savings policies, investing hundreds and even thousands each month for their childrens’ future education fees.

Plus the costs of weekend outings to indoor playgrounds, dining out and family vacations..

No wonder so many mothers lament that they have a tight budget and are unable to save for their retirement 😥

In the past, there used to be a saying in Chinese that 养儿防老, meaning bringing up your kid to take care of you in the future when you grow old.

However, nowadays most mothers (myself included) no longer expect our children to support us and return the favour. Instead, all we wish is for our children to be financially independent so we no longer need to worry about them.

“I would be happy if my kids can be independent when they grow up and take care of themselves”

Given this case, isn’t it all the more important that as mothers, we plan for our own future? To support ourselves financially and not depend on our children, or add to their burdens?

By the time we reach our retirement age, our children would probably be in their prime stage – planning their career paths, starting their family, with their own financial strains and liabilities.

I believe the last thing parents want is to become a burden to their children, especially when they are young and starting to take off in their careers and life.

Therefore we need to concurrently plan for our retirement while planning for children’s future.

So what can we do about this? How can mothers balance between saving for their retirement and their children’s future?

I recalled a video by an insurer, where a young man was featured by paying tribute to his parents during his wedding. When he was young, his parents did not give him the best holiday in Europe nor buy him many toys. Instead, they saved up for their retirement.

As a result he is now free to live his dreams without worrying about his parents. The tagline of this video is ‘The best gift you can give your children is a retirement plan for yourself.’

I strongly resonate with this message (I am not linked to the insurer by the way 😉).

I believe that our children can enjoy a happy childhood even without the exotic overseas holidays, costly outings or fancy parties. We can create close knit bonds with our children through simple family bonding activities that don’t cost a lot. The are also plenty of affordable family friendly holiday destinations to choose from. All it takes is a bit of creativity and a fun heart.

Childcare expenses are one of the highest cost for parents especially for those who send their children to high-end childcare centres like Mindchamps or Pats Schoolhouse. Premium childcare fees can cost as much as $1800/mth (more than a SMU education!). In contrast, choosing a government partner childcare centre caps the school fees at $800/mth before subsidies, which means up to $1000 savings per child per month! And it can still provide quality education, good learning environment and caring teachers.

With the additional money saved, you can grow for the future via investments or channelling it to build up your retirement income through an annuity plan. Check out more strategies to help women boost their retirement fund here. Now your children can be truly free to live their life without worries and you can enjoy your retirement too.

3. Know what you have

“My husband takes care of all the finances/insurance matters. He even files my taxes for me!” This is what a capable female TCM doctor said recently when I asked her about her financial health.

In today’s society, many women are educated, intelligent and capable, however when it comes to financial matters, some still choose to leave it to their spouse.

While this seems like a really convenient and easy option, it is important that as women, we know and take ownership of our finances.

I have come across multiple cases of women who trusted their spouse to take care of everything. However when the marriage, unfortunately, fell apart, they discovered to their shock that the family finances were in array, wrong investments had been made, there were no proper insurance in place or worse their children’s coverage had lapsed …

It became extremely challenging and financially stressful for the mothers to single-handedly pick up the pieces and get things back in order.

What you need to know about your finances:

- Your basic financial health – what’s the family’s net worth and cash flow. Is it healthy?

- Do you have the necessary insurance coverage in place?

- For stay home mums, make it a point to discuss with your spouse and plan for both your retirement. Your working spouse can consider topping up your CPF account for the future while saving on income tax at the same time. More about it here

I encourage couples to discuss their finances together because that helps to build mutual understanding and is an act of trust. Over time, it minimizes money disputes and strengthens the marriage.

If your spouse currently handles most of the money matters, my suggestion is to take a proactive stand to get involved or at least be curious to understand what’s going on. Who knows you can also provide some valuable inputs or ideas to improve the family’s finances!

Lastly,

By cultivating healthy financial habits, taking care of yourself and planning for your future, your children will also learn how to manage their finances well and be free to live with confidence and with a peace of mind.

To Your Success and Happiness,

Yong Hui